June 2022 NewsLetter

Management comments

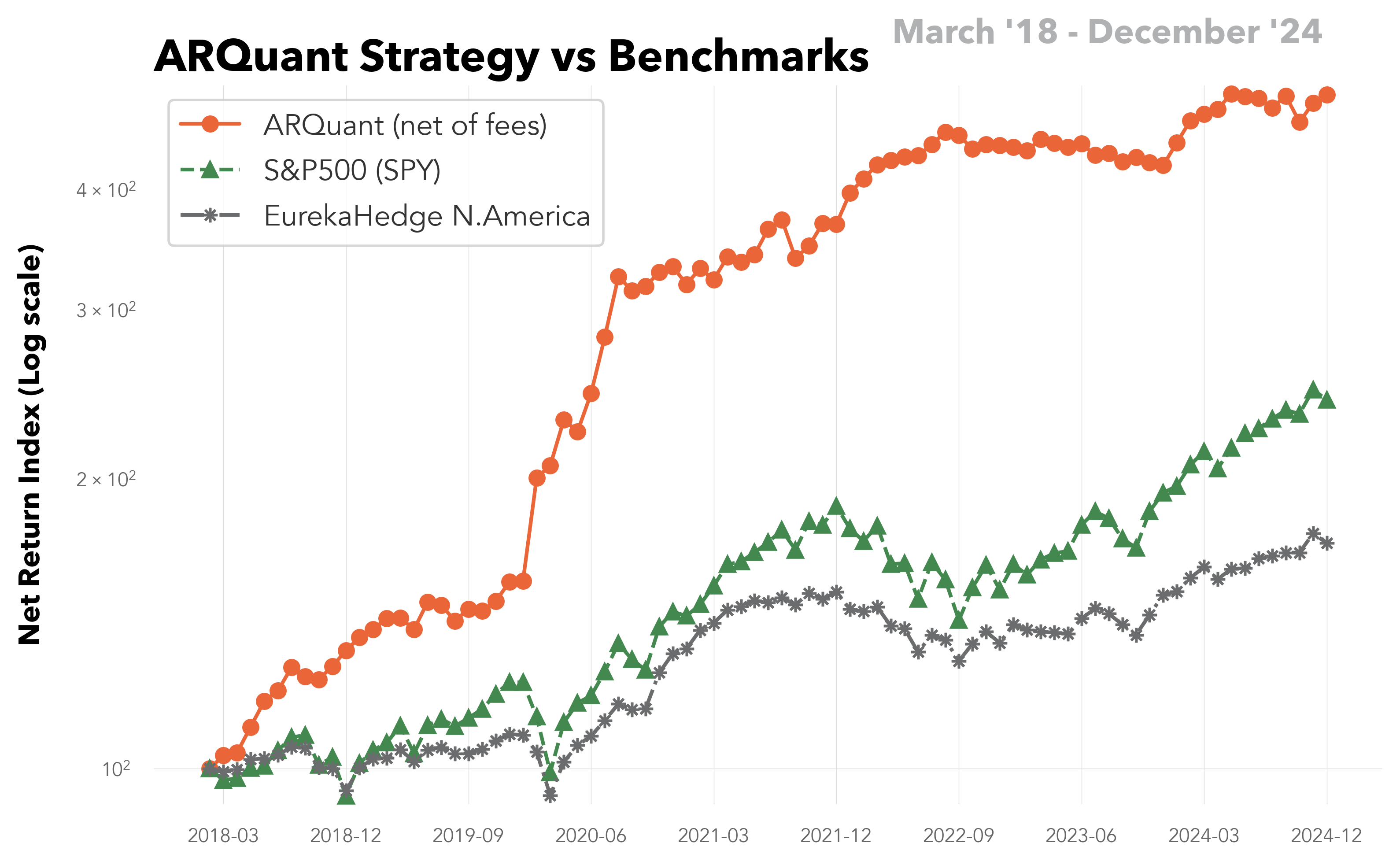

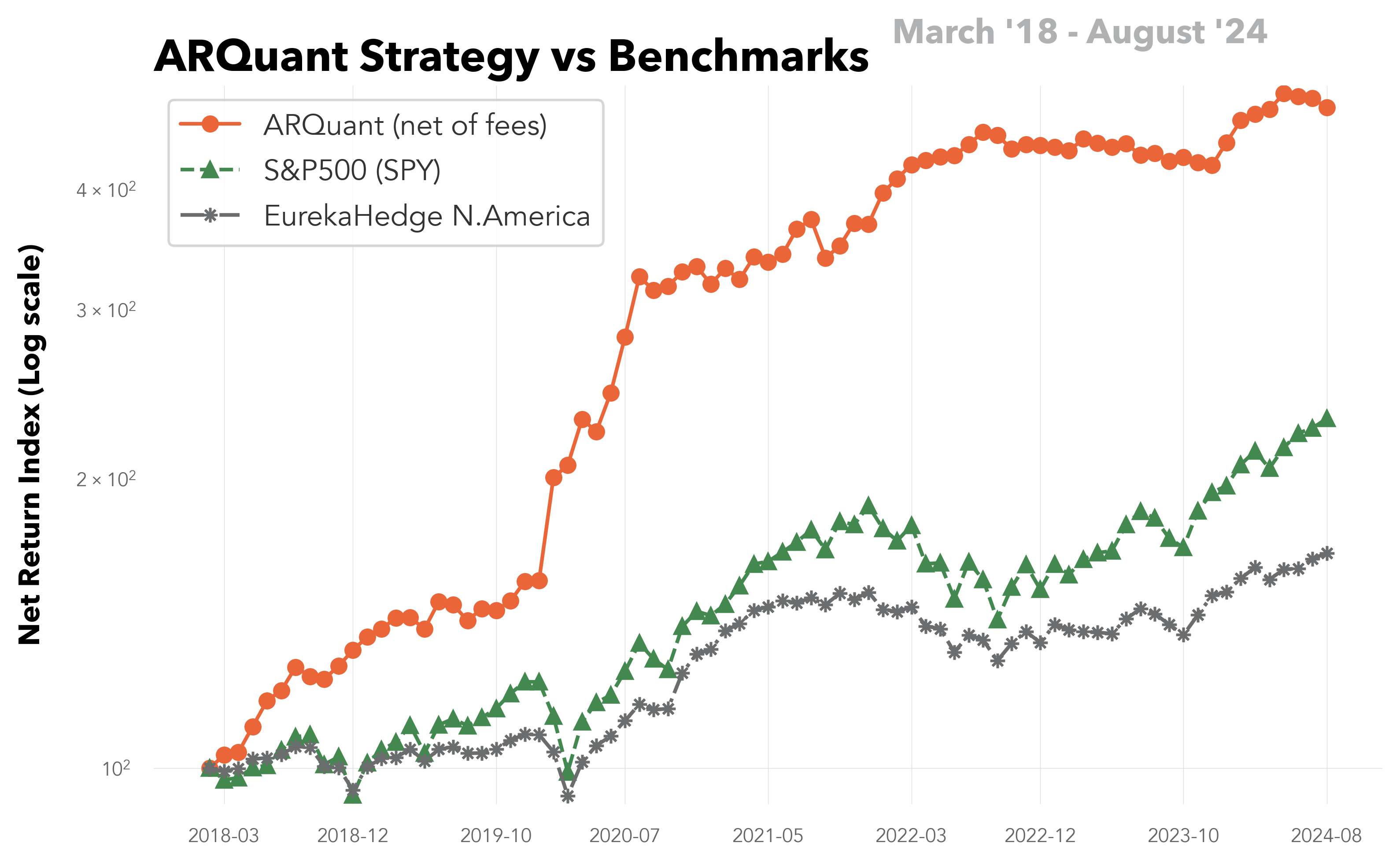

Returns generated by the ARQuant’s strategy in June was like a roller coaster that finally resulted with a modest net return of 0.3% per month which however was not too bad compared to S&P500 (-8.4% p.m.) and our benchmarks HFRI EH Quantitative Directional Index (-2.6% p.m.) and Eurekahedge North America Long Short Equities Hedge Fund Index (-5.0% p.m.). Our robot is able to generate alpha even in a such volatile market.

Despite a drawdown at the beginning of the month, the robot successfully predicted the market fall and generate impressive returns by 15th June, and even reached a new intraday high-water mark. Then the market started ups and downs which didn’t allow us to fix the success. Daily average of gross exposure was higher than in May (33% vs 22%). Net exposure was almost neutral (only 2%) on average however varied from +77% to -55% over the month.

Last Month

June 13 was the best day when daily return reached 3.5% and in three days the worst day of the month happened when a single day drawdown was -2.9%.

Year-to-Date (YTD)

January is still the best month of this year with 7.84% p.m. return (before fees), and June became

the weakest month with 0.72% p.m. return (before fees).

The full Newsletter can be found here: ARQuant Newsletter 2022-06

Warning: Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss. There is no guarantee that these investment strategies will work under all market conditions and each investor should evaluate their ability to invest for a long-term especially during periods of flat market or downturn in the market.

Warning: Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Derivatives may involve certain costs and risks such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss. There is no guarantee that these investment strategies will work under all market conditions and each investor should evaluate their ability to invest for a long-term especially during periods of flat market or downturn in the market.